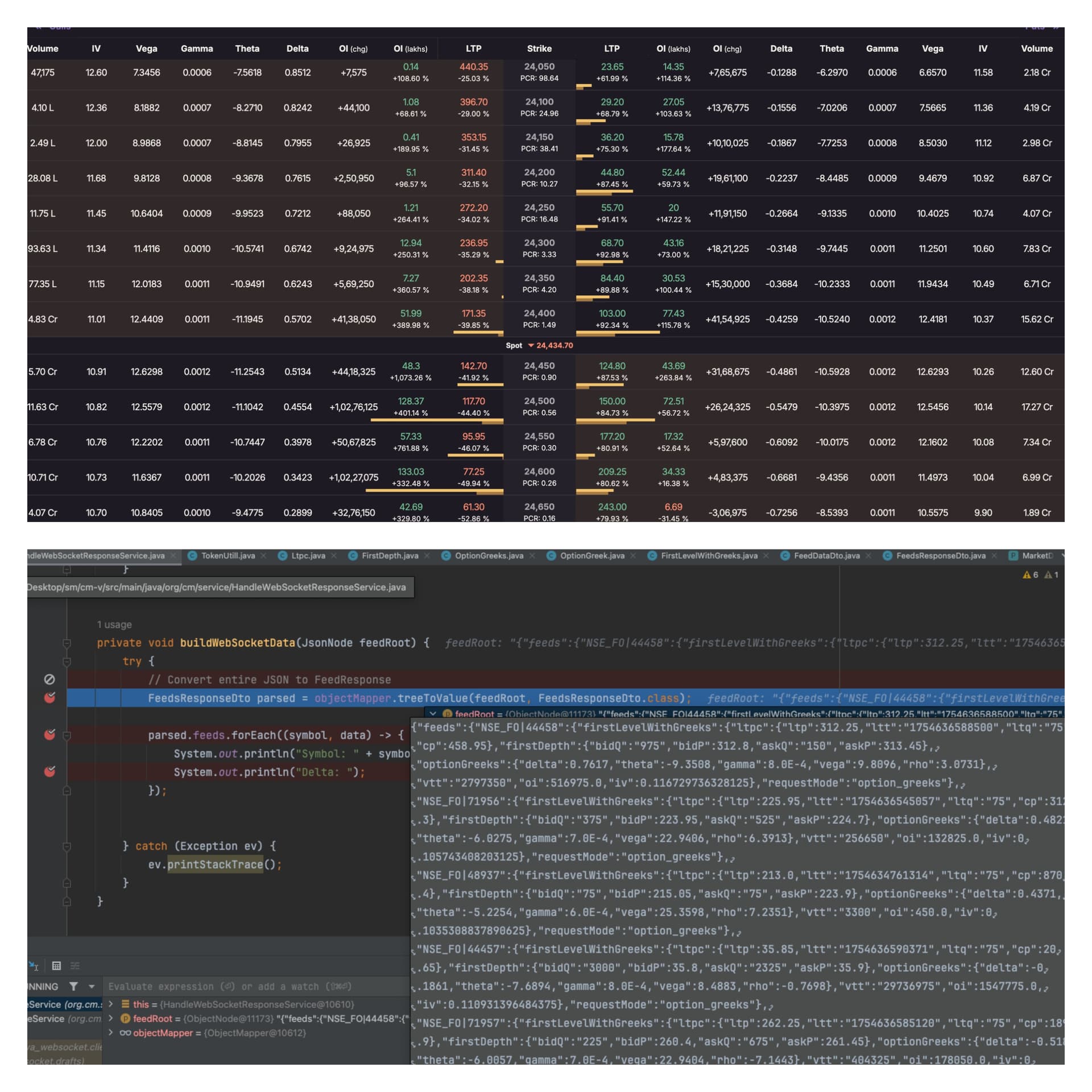

In one screenshot, there’s WebSocket data where the IV is mostly between 0.2 and 0.8.

On the other side, there’s your Upstox web option chain where the IV for the same strike price is around 10 to 13.

I’m not sure what internal calculations are happening, but if there aren’t any, then why is there such a major difference between the IV from the web option chain and the IV from the WebSocket data?

Hi @Ajay_22387638

The Implied Volatility (IV) values in the WebSocket feed and the UI are both correct — they are simply represented in different formats.

WebSocket: IV is provided in decimal format. For example, 0.13 means 13%.

UI: IV is displayed as a percentage, so the same value appears as 13.